Digital Envelope System vs Cash Envelopes: Which Works Better?

Digital Envelope System vs Cash Envelopes: Which Works Better?

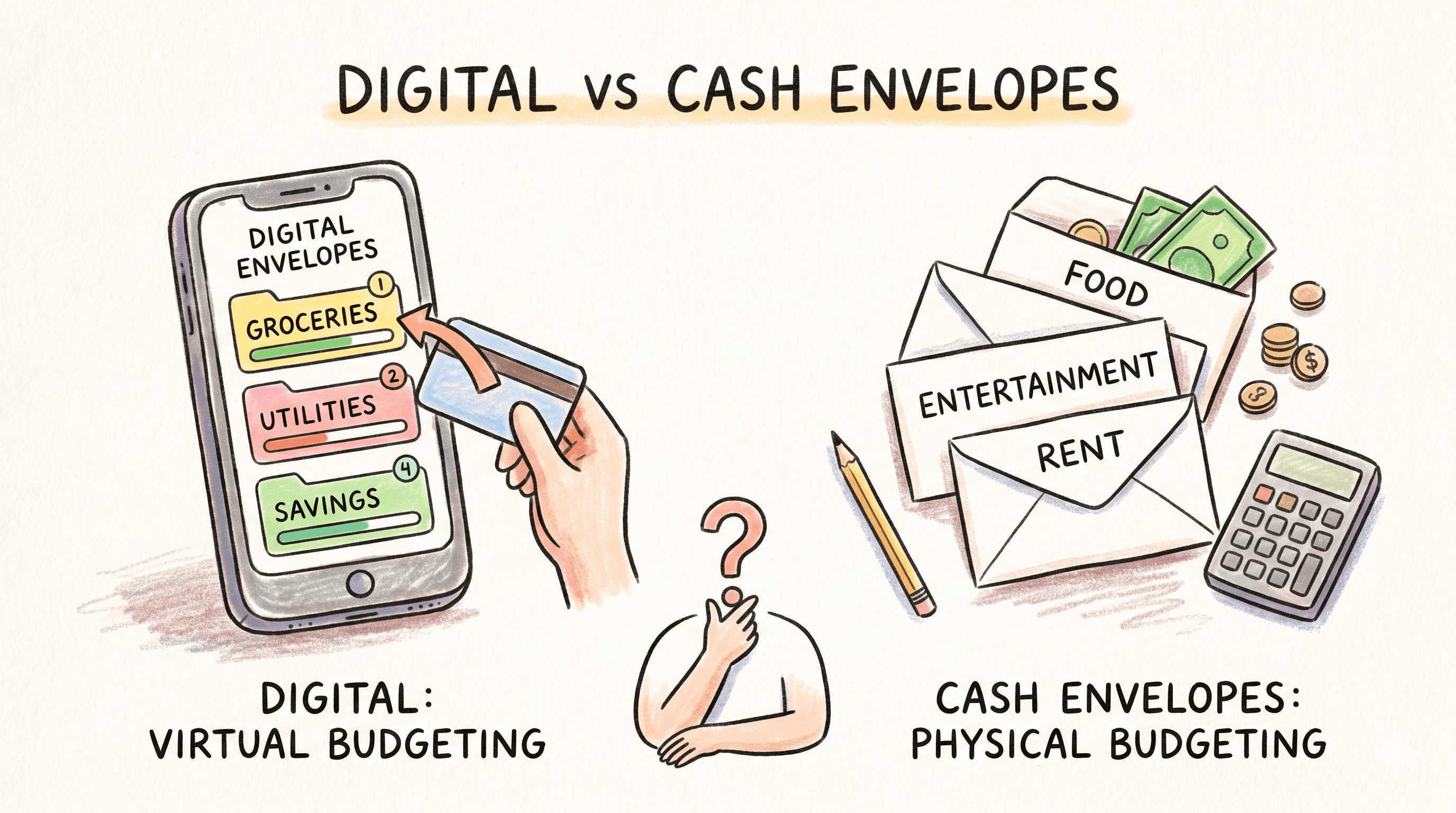

The envelope budgeting method has helped families control spending for generations. The classic approach uses actual cash in physical envelopes. But in 2026, most of our spending is digital—so should our envelopes be too?

Both systems use the same principle: divide money into categories and stop spending when a category is empty. The difference is in execution. Here's how to decide which works best for your family.

The Cash Envelope System

How It Works

- Withdraw cash after each paycheck

- Divide it into labeled envelopes

- Spend only from the appropriate envelope

- When empty, stop spending in that category

What You Need

- Envelopes or a cash envelope wallet

- Categories written on each

- A safe place to store them

- Discipline to use cash for purchases

Categories That Work Well With Cash

| Category | Why Cash Works |

|---|---|

| Groceries | Fixed location, cash-friendly |

| Dining out | Restaurants take cash |

| Entertainment | Most venues accept cash |

| Personal spending | Any purchase type |

| Kids' allowances | Teaches money physically |

| Coffee/treats | Small, frequent purchases |

Categories That Don't Work With Cash

| Category | Why Cash Doesn't Work |

|---|---|

| Online shopping | Can't use cash |

| Subscriptions | Auto-charged to card |

| Bills | Need auto-pay or checks |

| Gas (sometimes) | Pay-at-pump requires card |

| Large purchases | Safety concern |

Pros of Cash Envelopes

Tangible and visual Seeing money leave your hand creates an emotional connection that cards don't provide. Watching the envelope get thin is powerful.

No overspending possible You literally cannot spend more than what's in the envelope. No temptation. No "just this once." The limit is physical.

Simplified tracking No app needed. No checking balances. Just look in the envelope.

Privacy No digital footprint of your spending.

Teaches kids effectively Children grasp physical money better than numbers on screens.

Cons of Cash Envelopes

Inconvenient for modern life Most purchases today happen with cards or online. Cash doesn't work for these.

Security concerns Walking around with hundreds in cash is risky. Losing your wallet loses real money.

ATM fees Withdrawing cash frequently can cost money.

Splitting bills is awkward When the check comes, figuring out whose envelope pays what gets complicated.

No spending history Where did that $20 go? You won't remember.

Requires discipline to withdraw The system breaks if you don't regularly get cash.

The Digital Envelope System

How It Works

- Set up categories in a budgeting app

- Assign money to each category digitally

- Transactions are categorized (automatically or manually)

- App shows remaining balance per category

- When category is empty, stop spending

What You Need

- Budgeting app with envelope functionality

- Bank/card accounts linked

- Smartphone for access

- Regular review habit

How Digital Matches Physical

| Physical Action | Digital Equivalent |

|---|---|

| Put cash in envelope | Assign budget to category |

| Take cash from envelope | Transaction deducts from category |

| Check envelope | Check app balance |

| Move cash between envelopes | Transfer budget between categories |

| Empty envelope = stop | Zero balance = stop |

Pros of Digital Envelopes

Works everywhere Cards, online shopping, subscriptions—digital tracking handles all transaction types.

Automatic tracking Transactions import automatically from linked accounts. Less manual work.

Always accessible Check any category balance instantly from your phone.

Shared with partner Both partners see the same balances in real-time.

Spending history See where money went. Identify patterns over time.

Goal tracking Many apps include savings goals and progress visualization.

Security No physical cash to lose or have stolen.

Analytics and reports Understand your spending with charts, trends, and insights.

Cons of Digital Envelopes

Less tangible Numbers on a screen don't feel as "real" as cash leaving your hand.

Requires discipline differently Nothing physically stops you from overspending. You have to choose to stop.

Learning curve Apps require setup and habit building.

Technology dependent Phone dies? App glitches? Inconvenient moments.

Privacy concerns Your spending data exists somewhere.

Delayed transactions Some purchases take days to post, making real-time tracking imperfect.

Comparing Effectiveness

For Overspending Prevention

Winner: Cash

The physical limitation of cash provides a hard stop that digital can't match. When the envelope is empty, you're done—no workarounds.

However, digital works for disciplined individuals who respect the numbers.

For Modern Life Compatibility

Winner: Digital

Online shopping, subscriptions, and card-required purchases make cash-only nearly impossible for most families.

For Couples

Winner: Digital

Real-time shared access means both partners see the same picture. Cash requires constant coordination about who has which envelope.

For Learning and Awareness

Tie

Cash teaches through physical sensation. Digital teaches through data and patterns. Both create awareness—just differently.

For Long-Term Tracking

Winner: Digital

History, trends, reports. Understanding spending patterns requires data only digital provides.

For Simplicity

Winner: Cash

No apps, no logins, no learning curve. Just envelopes and money.

The Hybrid Approach

Many families find success combining both systems:

How Hybrid Works

Use digital for:

- Overall budget tracking

- Fixed expenses (bills, subscriptions)

- Online purchases

- Income allocation

- Savings tracking

Use cash for:

- High overspend-risk categories

- Dining out

- Entertainment

- Personal spending

- Groceries (if preferred)

Setting Up a Hybrid System

Step 1: Digital foundation Set up all categories in your budgeting app.

Step 2: Identify cash categories Pick 2-4 categories where you tend to overspend.

Step 3: Withdraw for those categories After budgeting digitally, withdraw cash for those specific categories.

Step 4: Track both Digital handles most tracking. Cash categories show as one withdrawal.

Example Hybrid Budget

| Category | Method | Amount |

|---|---|---|

| Rent | Digital (auto-pay) | $1,500 |

| Utilities | Digital | $200 |

| Groceries | Cash envelope | $600 |

| Transportation | Digital | $300 |

| Dining out | Cash envelope | $200 |

| Entertainment | Cash envelope | $100 |

| Personal (each) | Cash envelope | $150 |

| Savings | Digital (auto-transfer) | $400 |

Cash categories: $1,200 (withdraw monthly) Everything else: tracked digitally

Choosing Your System

Choose Cash Envelopes If:

- You struggle with overspending on cards

- You're a visual/tactile learner

- Your spending is mostly local and in-person

- You want maximum simplicity

- You're teaching kids about money

- You've tried apps and they don't stick

Choose Digital Envelopes If:

- Most of your spending is online or card-based

- You budget with a partner

- You want detailed spending analysis

- You travel frequently

- You're comfortable with apps

- You need flexibility in how you pay

Choose Hybrid If:

- You want digital convenience with cash discipline

- You overspend in specific categories only

- You budget as a couple

- You want the best of both worlds

- Pure cash feels impossible but pure digital lacks teeth

Making Each System Work

For Cash Success

- Choose the right categories - Only use cash where it makes sense

- Set a withdrawal schedule - Same day each pay period

- Keep it safe - Don't carry all envelopes everywhere

- Have a backup - Emergency card for true emergencies

- Partner coordination - Who carries what, when

For Digital Success

- Check balances before spending - Make it a habit

- Categorize daily - Don't let transactions pile up

- Use notifications - Get alerts when categories are low

- Trust the system - Stop when it says stop

- Weekly reviews - Stay connected to the numbers

For Hybrid Success

- Be consistent - Same categories cash, same digital

- Reconcile regularly - Cash categories need manual entry

- Don't double-count - The cash withdrawal is the envelope

- Partner alignment - Both understand which is which

- Evaluate monthly - Is the split working?

Common Questions

"Can I use multiple cards with digital envelopes?"

Yes. Link all cards and accounts. Transactions from any source categorize into your envelopes.

"What about cash back or rewards?"

Digital tracking lets you use rewards cards while still maintaining envelope discipline. You can't get rewards with cash.

"How do I handle shared expenses with cash?"

Split the cash envelope, or one partner carries it and reimburses. It's awkward but workable.

"What if my cash envelope is empty but I need groceries?"

Transfer from another envelope (digitally or physically), or wait. The system only works if you respect the limits.

"How do I categorize cash purchases digitally?"

Enter them manually, or use the withdrawal as a lump "cash spending" category you manage physically.

Real Family Examples

The All-Cash Family

"We tried apps and never checked them. Cash changed everything. We have 8 envelopes. When dining out is empty, we cook. Simple."

The All-Digital Family

"With two kids in activities and all our shopping online, cash was impossible. Our app syncs instantly—we both always know where we stand."

The Hybrid Family

"I use cash for my 'danger zones'—eating out and Target runs. Everything else is digital. I've saved $400/month just from the cash limits on those two categories."

The Bottom Line

There's no universally "better" system. There's only what works for your family.

Cash envelopes provide unmatched physical limits for overspenders. Digital envelopes provide convenience and tracking for modern life. Hybrid combines strengths of both.

The best system is the one you'll actually use consistently. Start somewhere. Adjust as you learn. The method matters less than the practice.

What matters is that every dollar has an envelope—physical or digital—and that you respect the limits you set.

Choose your system. Start this month. Master your money.

Written by

Rafał GawlikFounder of FamilyJar

Rafał Gawlik is the founder of FamilyJar, and a husband and father based in Kraków, Poland. He writes about family budgeting, the envelope method, and building financial security as a couple — drawing on the real-world workflows behind the FamilyJar app and his own experience running a household budget.

Related Articles

Envelope Budgeting for Beginners: Your First Month Step by Step

New to envelope budgeting? This beginner's guide walks you through your first month, from setting up categories to tracking spending the easy way.