Envelope Budgeting for Beginners: Your First Month Step by Step

Envelope Budgeting for Beginners: Your First Month Step by Step

Envelope budgeting is the simplest, most intuitive budgeting method ever created. It's been helping families manage money for generations—and it works just as well today.

The concept is beautifully simple: divide your money into envelopes for different spending categories. When an envelope is empty, you stop spending in that category. That's it.

If you've struggled with other budgeting methods, this might be the one that finally clicks. Here's your complete guide to starting envelope budgeting. For more depth, also check out our Complete Guide to Envelope Budgeting.

What Is Envelope Budgeting?

The Original System

In the days before credit cards, families literally put cash into labeled envelopes:

- Groceries: $400

- Gas: $150

- Entertainment: $100

When you needed groceries, you took money from the groceries envelope. When that envelope was empty, you stopped buying groceries (or borrowed from another envelope).

Why It Works

Visual and tangible: You see exactly what's left Self-limiting: Can't overspend what isn't there No tracking required: The envelope does the math Flexible: Move money between envelopes as needed Simple: Anyone can understand it immediately

Modern Envelope Budgeting

Today, most envelope budgeting is digital. Apps replace physical envelopes, but the principle is identical:

- Assign money to categories

- Track spending against each category

- When a category is empty, stop spending

Digital offers advantages: no cash withdrawals, automatic transaction tracking, better security, and always knowing your balance anywhere.

Before You Start: Gather Your Information

Know Your Income

List all income sources for the month:

- Salaries (after tax)

- Side hustles

- Other regular income

Total monthly income: $______

Know Your Bills

List fixed monthly expenses:

- Rent/mortgage

- Utilities

- Insurance

- Car payment

- Subscriptions

- Minimum debt payments

Total fixed expenses: $______

Know Your Spending

Look at last month's bank and credit card statements:

- What did you spend on groceries?

- How much on dining out?

- Gas and transportation?

- Entertainment and shopping?

Don't judge—just observe. This is your baseline.

Setting Up Your Envelopes

Step 1: Create Your Categories

Start simple. You can always add more later.

Essential categories for beginners:

| Category | Type | Notes |

|---|---|---|

| Rent/Mortgage | Fixed | Same every month |

| Utilities | Variable | Estimate average |

| Groceries | Variable | Your control |

| Transportation | Variable | Gas, transit, parking |

| Dining Out | Discretionary | Easy to cut if needed |

| Personal | Discretionary | Guilt-free spending |

| Household | Variable | Supplies, minor repairs |

| Savings | Fixed | Pay yourself first |

Add as needed:

- Childcare

- Medical

- Clothing

- Entertainment

- Kids' expenses

- Pets

Step 2: Assign Dollar Amounts

This is where the magic happens. You're telling every dollar where to go before the month begins.

Start with fixed expenses: These don't change, so assign them first.

| Category | Amount |

|---|---|

| Rent | $1,500 |

| Car payment | $350 |

| Insurance | $200 |

| Subscriptions | $50 |

Then savings: Pay yourself before discretionary spending.

| Category | Amount |

|---|---|

| Emergency fund | $200 |

| Savings goals | $150 |

Then variable necessities: Estimate based on past spending.

| Category | Amount |

|---|---|

| Groceries | $600 |

| Utilities | $200 |

| Gas | $150 |

| Household | $100 |

Finally, discretionary: What's left goes here.

| Category | Amount |

|---|---|

| Dining out | $200 |

| Entertainment | $100 |

| Personal | $150 |

Step 3: Make Sure It Balances

Income: $4,500 Total envelopes: $4,450 Buffer: $50

Your envelopes should equal your income (or slightly less for a small buffer). If they exceed income, you must cut something.

Your First Month: Week by Week

Before the Month Starts

Set up your system:

- Choose your tool (app, spreadsheet, or actual envelopes)

- Create all categories

- Enter your income

- Fund each envelope

Review with your partner: If budgeting with someone, align on amounts before starting.

Week 1: Learning Mode

Focus on tracking, not perfection.

Every time you spend money:

- Note the amount

- Assign it to an envelope

- See the remaining balance

That's it. Just build the habit.

Common week 1 discoveries:

- "I spend more on coffee than I realized"

- "Groceries went faster than expected"

- "I forgot about that recurring charge"

Don't panic. This is learning.

Week 2: First Adjustments

By now, some envelopes might be running low.

If an envelope is empty:

- Borrow from another envelope (transfer)

- Or stop spending in that category

If an envelope has lots left:

- You budgeted too high

- Or you're being careful (good!)

Make notes: "Need more in groceries next month" "Can probably reduce dining out budget"

Week 3: The Squeeze

This is where envelope budgeting proves itself. It's late in the month, some envelopes are tight, and you have to make choices.

The envelope forces decisions:

- Grocery envelope has $75 left? Plan simple meals.

- Entertainment is empty? Find free activities.

- Personal money gone? Wait until next month.

This isn't deprivation—it's intentionality. You're making conscious choices instead of mindlessly overspending.

Week 4: Finishing Strong

End of month review:

- Which envelopes were over?

- Which had money left?

- What surprised you?

- What will you adjust next month?

Roll over or restart:

Some people start fresh each month. Others roll over remaining balances. Both work—choose what motivates you.

Envelope Budgeting Rules

The Golden Rule

When the envelope is empty, stop spending in that category.

This is the whole system. Everything else is details.

The Flexibility Rule

You can move money between envelopes.

Life happens. Moving $50 from entertainment to groceries is fine. The budget serves you, not the other way around.

The Honesty Rule

Every expense goes in an envelope.

No "off-budget" spending. No pretending that purchase didn't happen. Track everything.

The Planning Rule

Fund envelopes before spending.

At the start of the month (or when you're paid), divide money into envelopes first. Spending happens second.

Common Beginner Mistakes

Mistake 1: Too Many Categories

Starting with 20+ categories overwhelms you. Begin with 8-12, then add more once the system is comfortable.

Mistake 2: Unrealistic Amounts

If you've been spending $800 on groceries, budgeting $400 will fail. Start close to reality, then reduce gradually.

Mistake 3: Forgetting Annual Expenses

Car registration, insurance renewals, holiday gifts—these need envelopes too. Divide annual costs by 12 and save monthly. Learn more about this in our guide to sinking funds for families.

Mistake 4: No Personal Money

If neither partner has guilt-free spending money, the budget feels suffocating. Include personal envelopes for each adult.

Mistake 5: Giving Up After One Bad Month

Your first month won't be perfect. Neither will your second. The system works when you stick with it and adjust. For a full breakdown of what can go wrong, see Envelope Budgeting Mistakes: 10 Errors That Derail Your Budget.

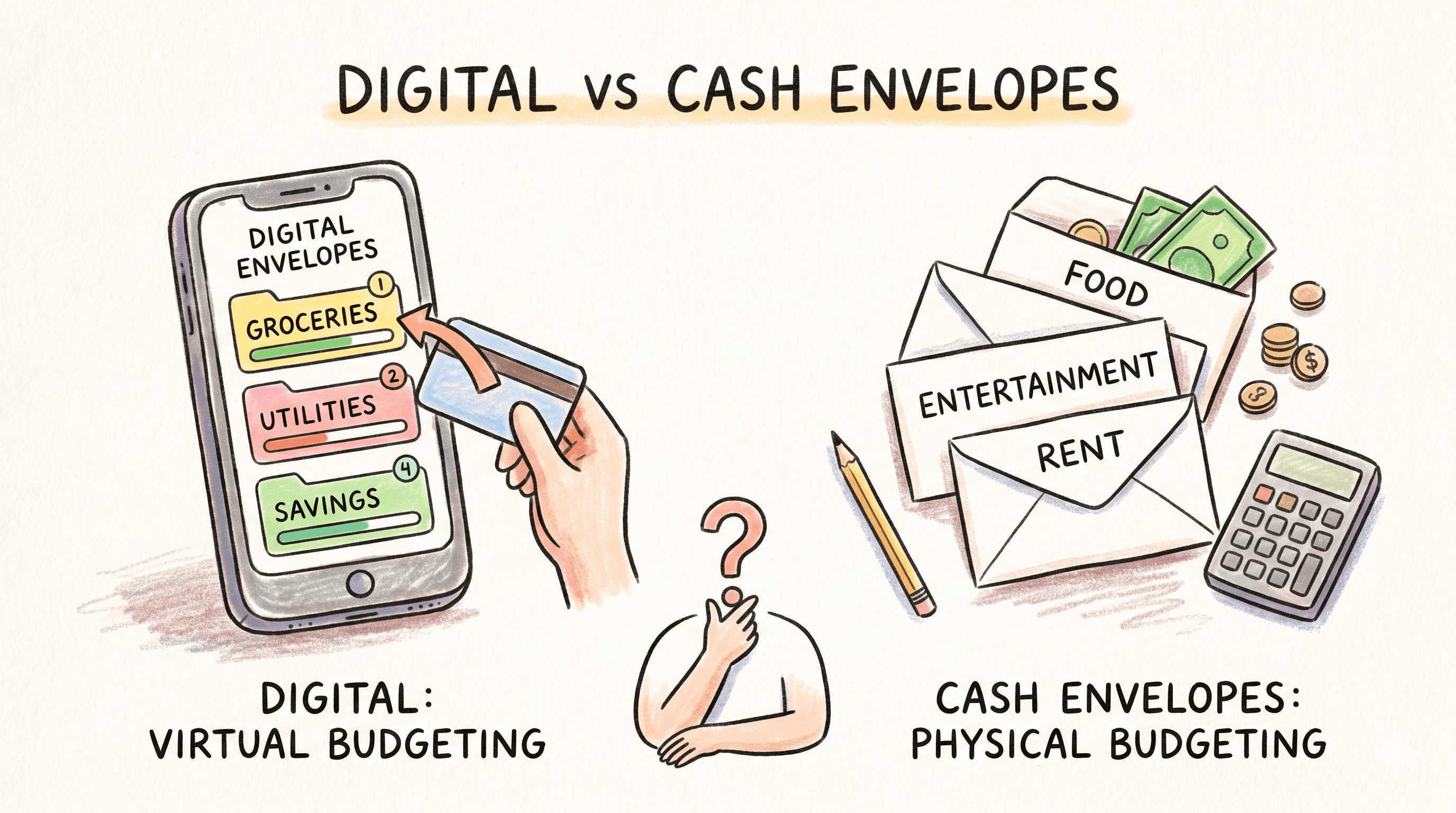

Physical vs. Digital Envelopes

Physical Cash Envelopes

Pros:

- Extremely tangible

- No app needed

- Forces cash-only discipline

- Visual satisfaction

Cons:

- Inconvenient for online purchases

- Security risk

- Can't track history easily

- Splitting bills is awkward

Best for: Visual learners, those struggling with overspending

Digital Envelope Apps

Pros:

- Works with cards and accounts

- Automatic transaction import

- History and reporting

- Always accessible

- Partner sharing built-in

Cons:

- Less tangible

- Requires app learning

- Can feel abstract

Best for: Modern life, couples, those comfortable with technology

Hybrid Approach

Use cash envelopes for overspending categories (dining out, entertainment) and digital for everything else. Learn more about both approaches in Digital vs Cash Envelopes.

Envelope Budgeting for Couples

For a deep dive into budgeting as a team, see Envelope Categories for Couples.

Shared Categories

Both partners see and spend from:

- Groceries

- Household

- Dining out

- Family entertainment

Personal Categories

Each partner gets their own envelope:

- Personal spending (His)

- Personal spending (Hers)

This autonomy prevents micromanagement while maintaining overall budget alignment.

Regular Check-Ins

Meet weekly to review:

- Where are we in each envelope?

- Any big purchases coming up?

- Adjustments needed?

Need help structuring these conversations? Read our guide to family budget meetings.

The "No Judgment" Zone

Personal envelopes are guilt-free. Don't criticize how your partner uses their personal money.

Building Your Envelope Habit

Daily

- Log any cash transactions

- Check envelope balances before buying

Weekly

- Review all envelopes

- Check for unassigned transactions

- Quick partner check-in

Monthly

- Evaluate what worked

- Adjust amounts for next month

- Celebrate wins

Make It Easy

- Set up phone notifications

- Check your app during morning coffee

- Link tracking to existing habits

After Month One: What's Next?

Month 2: Refinement

- Adjust envelope amounts based on Month 1

- Add or remove categories as needed

- Build consistency

Month 3: Optimization

- Start tracking spending patterns

- Identify where you can cut

- Increase savings contributions

Month 6: Automation

- System becomes natural

- Spending aligns with values

- Stress decreases significantly

Year 1: Transformation

- Financial goals being achieved

- No more end-of-month panic

- Complete control over money

The Envelope Budgeting Mindset

This isn't about restriction—it's about intention.

Every dollar has a job before the month begins. You decide what matters. When money runs out in one area, you're not failing—you're succeeding at staying within your plan.

The envelope that's empty isn't a problem. It's the system working exactly as designed.

Start Today

You don't need anything fancy to start envelope budgeting. A notebook and pen work. Actual envelopes work. A spreadsheet works. Apps work.

What matters is starting.

This week:

- List your income

- Create 8-10 categories

- Assign amounts

- Track every purchase

Your first month won't be perfect. That's not the point. The point is learning where your money goes and taking control.

Millions of families have used envelope budgeting to get out of debt, build savings, and achieve financial peace. You can too.

Open your first envelope. Your journey to financial clarity starts now.

Written by

Rafał GawlikFounder of FamilyJar

Rafał Gawlik is the founder of FamilyJar, and a husband and father based in Kraków, Poland. He writes about family budgeting, the envelope method, and building financial security as a couple — drawing on the real-world workflows behind the FamilyJar app and his own experience running a household budget.

Related Articles

Digital Envelope System vs Cash Envelopes: Which Works Better?

Compare digital and cash envelope budgeting systems. Discover which approach fits your lifestyle, with pros, cons, and hybrid strategies.

The Complete Guide to Envelope Budgeting for Families

Learn how envelope budgeting can transform your family's finances. Discover the proven method that helps couples manage money together with transparency and purpose.